‘Money Without Work’ 7: Betting Psychology

It is perhaps the greatest paradox in the investment world that many consistently profitable money managers have a large percentage of losing clients, writes Russell Clarke. I recently saw the records of a very successful US Hedge Fund, that showed over 40% of their lifetime client base had actually lost money while investing with the fund! This was a fund that had a relatively consistent record of double digit annual gains over decades. This rather odd story is by no means an isolated incident, it is repeated within many successful funds.

So, what causes this phenomenon? Bad timing and illogical emotion probably covers the answer. It is human nature to be tempted to buy into an investment when it is doing well and sell when doing badly. Jack Schwager in his cult classic, Market Wizards, sums up “the common dual tendency of many people to initiate an account after a manager has already had a large winning streak and to liquidate in the midst of a drawdown is the single biggest blunder investors make”. Clearly, if the path to riches was as simple as to just invest in a fund that was currently outperforming, we would all be rich.

The Turtles Story

In 1984 a man called Richard Dennis had a wager with his financial trading partner, William Eckhardt, that he could train a selected number of people (later to be termed The Turtles) to trade profitably in the financial marketplace, with no prior financial trading experience. It was a classic Nature v Nurture experiment. Over a thousand people responded to simple classified advertisements placed in The International Herald Tribune, Barrons and The Wall Street Journal. From these, around 40 were interviewed and a dozen or so were initially chosen.

The Turtles were given just two weeks training and were then allowed to trade with real money, strictly following the relatively simple systems and rules taught them by Dennis and Eckhardt. This story is almost folklore in financial circles, albeit a little cultish. The systems they were taught were simple and took up very little of each day. They traded at simple desks in a non-descript office where the most used piece of equipment was a ping-pong table!

The Turtles were “trend-following” traders. Trend followers wait for a market to move and then follow it. The aim is to capture the majority of a trend, either up or down. The doyen of trend followers was Richard Donchian; as far back as 1960, he encapsulated the philosophy into a brief rule, “When the price moves above the high of the previous two weeks, cover your short positions and buy. When the price breaks below the low of the two previous weeks, liquidate your long position and sell short.”

The Turtles themselves entered markets on breakouts. For example, if a contract made a 55 day breakout (i.e. higher than at any time in the past 55 days), it was a buy. Similarly, if it broke to the downside they would sell. They were buying rising markets and selling falling markets….the age old wisdom of “buy low and sell high” turned on its head! The Turtles also used a shorter term breakout system that operated over 20 days. Each turtle was allowed to use either system, or both, or any combination of the two.

In terms of staking, the Turtles were taught about risk management and how much to risk on each trade. This was done by calculating the daily volatility in each market. Again it was a relatively simple calculation. Given this, it is perhaps surprising to note the differences in returns made in that first year by the Turtles. Jim Melnick produced an outstanding +102% in 1984, wheras Liz Cheval managed a loss of -21% over that same initial 12 month period. The same methodology brought very different results with cognitive behaviour and biases playing a major role.

The story itself is a fascinating one and I cannot do it justice in such a short article, but the result was that Dennis was proven correct as a number of the Turtles went on to take their place among the most successful traders on Wall Street over the following three decades.

Turtles and Betting

How does this relate to betting? As a boy, I was both fascinated and perplexed, in equal proportions, by The Sporting Life Naps Table. Each year less than 20% of the full-time racing journalists in the competition ever managed a level stake profit, and every year it was a different 20%! Their results looked completely random. The conclusion that screamed at me was that fundamental/subjective analysis of form (as practised by virtually every racing journalist) was very difficult to profit from, and individuals, over a lengthy period of time, are just not suited to profiting from their own opinion. To be entirely fair, they were also presenting their tips without any knowledge of the price of the horses they were selecting.

Given this, why is fundamental/subjective analysis of form, going, distance, trainers, so popular? Because most people know no other way? Because we need to feed our ego (my opinion is superior to your opinion)? Because it seems the most logical thing to do? Probably it is a mixture of these reasons and maybe others that I have not considered.

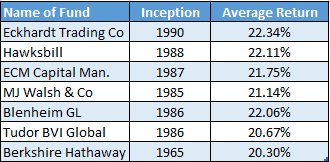

Returning to the financial world where information is available 24/7 and is far more public than in sports betting, I researched the published results of the most successful funds. To eradicate luck and optimisation, I looked for exceptional performance over a lengthy period of time. I chose 20 years to cover bull and bear markets and a myriad of economic conditions. I settled on 20%+ pa average returns over the 20 years. Unsurprisingly, with the bar set so high, only seven funds qualified.

Of these seven funds, four are systematic investing funds. The definition of systematic would be “rule-based trading”. One of the others (Paul Jones' Tudor) certainly uses a systematic approach, even if it is not strictly rule-based. And, of course, Berkshire Hathaway is the investment vehicle of Warren Buffet! That more than half of this most exclusive league table is made up of systematic investing funds is even more remarkable when you know that less than 1% of all funds available worldwide operate on a systematic basis.

So, why does an objective approach achieve superior results to a subjective one? The major reason is Psychology. The brain is not the rational, calculating machine that we like to believe. Over its evolution it has developed many shortcuts, biases and downright bad habits. Some of these would have helped early humans (fight or flight), but they create problems for us today. In addition, some of the brain’s flaws may result from socialisation rather than instinct. As a result of both nature and nurture, the brain can be a deceptive guide for rational decision making.

The brain’s inadequacies have been rigorously studied by social scientists. In the world of economics and investment, behavioural economists question the basic assumption of human beings as rational decision makers. They are correct to do so because the evidence is overwhelming. The insights presented here, primarily from the world of finance, are equally relevant to sports betting. Investments are no more than bets on the financial markets and sports bettors can learn plenty from the more sophisticated financial world.

"Overconfidence killed the caterpillar"

Our brains are programmed to make us feel overconfident. This has been tested in numerous studies. For example, people were asked to guess the weight of a London double decker bus; but, rather than a precise figure, give a range within which they were 90% confident they had the correct answer. Time and again, they fell into the trap of quoting too narrow a range and thus missing the correct answer. Most of us are unwilling to reveal our ignorance by specifying a very wide range.

We prefer to be precisely wrong than vaguely correct.

Overconfidence in our own abilities spills over into over-optimism. This can have dangerous consequences when developing strategies, as these are based on what may happen and, too often, are unrealistically precise and over-optimistic estimates of the uncertainties.

Mental Accounting

This term was first coined by a pioneer of behavioural economics called Richard Thaler. He defined Mental Accounting as “the inclination to categorise and treat money differently, depending on where it comes from, where it is kept, and how it is spent.” For example, a gambler who loses his winnings, typically feels he hasn’t really lost anything, despite the fact he would have been richer had he stopped when he was ahead. This can cause problems such as erratic staking.

Status Quo Bias

Nothing to do with Francis or Rick! In a classic experiment conducted by Samuelson and Zeckhouser, students were given a hypothetical inheritance. Some were given the inheritance in the form of a low risk profile portfolio, others were given it in the form of a high risk profile portfolio. Both sets showed a reluctance to change the allocation. The rational choice would have been to re-balance the portfolios, but the students largely chose not to change. The fear of changing comes from aversion to loss.

A similar bias is the Endowment Effect, which is an irrational desire to hang on to what you own. To demonstrate this, Thaler gave students a mug emblazoned with their University Logo. On average, the students demanded $5.25 before they would sell. However, students without the mug were only willing to pay $2.75 to acquire one.

Both the Status Quo Bias and the Endowment Effect make for poor decision making.

Anchoring

A well known bias. Present the brain with a number and ask it to make an estimate of something completely unrelated, the estimate will be anchored by the original number.

A classic example of this is when two groups were asked at what age Ghandi died. The first group were asked if he died before or after age nine and the second group were asked if he died before or after age 140. Both examples were obviously wrong, but, the anchor effect made the first group guess an average age of 50 and the second group an average age of 67.

Anchoring can be seen in price negotiations (buyer starts low, seller starts high), or advertising a retail price. Fund managers advertise past performance, and, despite the fact that there is very little correlation between past performance and future performance, it is anchored in the consumer's mind.

Related to Anchoring is the need for really statistically robust numbers for predicting the future. A great example is Equities. Anyone looking at the 1980’s and 1990’s would have a double digit per annum return firmly anchored. But the noughties brought a negative return! And the 60’s and 70’s returned a miserable 2% per annum. Double digit returns have been achieved in only four of the past 13 decades. So beware of a mere 20 year track record!!

Sunk Cost

Otherwise known as “throwing good money after bad”. Why do we do it? Loss aversion is the broad answer and the current trend for “kicking the can down the road” by the governments of the world is a classic example. Bailing out countries such as Greece (that can never repay their debts) is deemed preferable to accepting the inevitable loss today.

On a more personal level, you buy shares in ABC for £1, but the price falls to 70p….do you accept the loss? For most people, the answer is “no”. Indeed, Anchoring kicks in (i.e. you may sell if the price recovered to £1, despite the fact at £1 you originally felt the share was a buy).

Herding Instinct

The desire to conform to the opinions and behaviour of others is a fundamental human trait and an accepted principle of psychology. We don’t mind being wrong, if everyone else is also wrong! To quote Warren Buffet, “as a group, lemmings may have a rotten image, but no individual lemming has ever received bad press”.

For punters, the herding instinct is difficult to resist. Give yourself half a chance, and stop reading the Racing Post! [Read geegeez.co.uk instead! - Ed.]

False Consensus

The tendency to over-estimate the extent to which others share your views or beliefs. This happens for a number of reasons, including:

- Confirmation Bias is the tendency to seek out opinions and facts that support your own beliefs (readership of newspapers with a certain political bias is a good example, the twitter accounts you follow perhaps another).

- Selective Recall is the habit of only remembering facts and experiences that reinforce our assumptions or beliefs.

- Biased Evaluation is the quick acceptance of evidence that supports your own hypothesis, whilst reserving rigorous analysis for any contrary opinion. And, finally...

- Groupthink is the pressure to agree with others in team-based cultures.

False Consensus is a very dangerous psychological trait in either financial investments or in betting.

An awareness of the brain's flaws and psychological traits can be a major factor when attempting to be successful in any form of investment/betting. The human brain itself makes it unsuitable as a primary tool for financial analysis. Therefore attempting to profit from betting using a subjective approach, whilst emotionally satisfying when proven correct, is fraught with dangers and difficulties that can be potentially circumvented if one adopts and maintains a 100% objective, rule-based approach.

I realise that here at Geegeez the majority will follow a hybrid of objective and subjective methods for bet selection. The purpose of these articles is not to change your approach. Rather, it is to highlight mathematically optimal situations in which to bet (either objectively or subjectively). This particular article is designed to highlight some of the more common psychological ‘traps’ that can scupper even the most advantageous EV+ strategy. They are especially problematic when variance takes a turn for the worse!

- RC

CLICK HERE FOR THE FINAL PART, 'MONEY WITHOUT WORK 8: LOGISTICS'